The first close of Toronto-based GreenSky Ventures’ sixth fund puts it in the 99th percentile of all Canadian venture capital (VC) firms over the past decade.

The early-stage VC firm announced a more than $15-million CAD first close of Fund VI from a group of limited partners (LPs) that includes undisclosed family offices and high-net-worth individuals, many of which are returning.

“We do think that if we can minimize the number of failures, that’s one way you could really contribute to growing attractive long-term returns.”

Marian Hoffmann, GreenSky

GreenSky ultimately aims to raise a total of between $20 million and $25 million by the end of 2024 for its sixth fund, which it expects to be its largest to date, topping its $21-million Fund V.

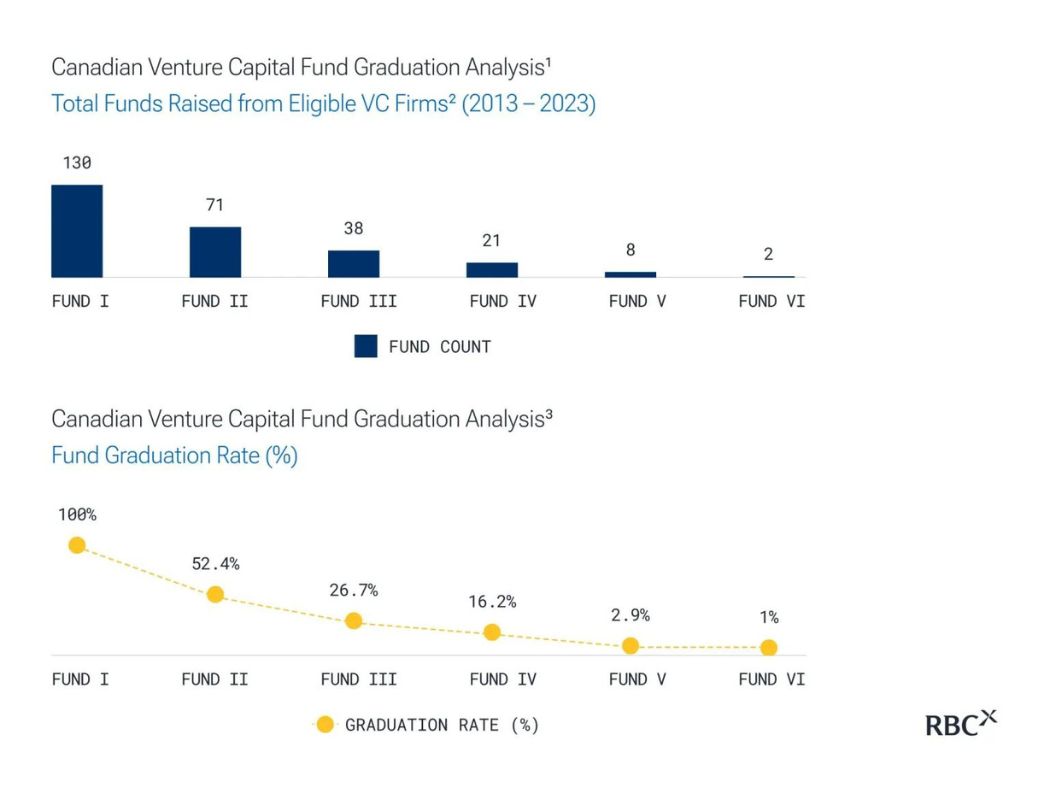

Reaching a sixth fund puts GreenSky in some rare company. According to recent research from RBCx, only one percent of Canadian VC firms have graduated to a sixth fund (excluding all opportunity, continuity, and alignment funds) over the last 10 years.

GreenSky managing partner Marian Hoffmann believes the firm has gotten to this point—and done so amid such a tough VC fundraising environment—thanks to its consistent strategy, team continuity, and performance.

Fund VI will look a lot like GreenSky’s prior funds, with a focus on investing in Canadian business-to-business deep technology and enterprise software startups at the seed and Series A stages and building a concentrated portfolio of eight to 12 companies that fit this bill.

“We’re really proud of the results that we’ve been able to generate following this strategy,” Hoffmann told BetaKit in an exclusive interview. “We’ve been doing it for almost a decade now, so [we’re] just going to keep doing what we’ve been doing.”

GreenSky was founded in 2010 by managing partner Mike List as a company that primarily invested its own capital and money drawn from its immediate network, and took equity from businesses in exchange for advisory services, including help fundraising. In 2015, GreenSky transitioned away from this advisory model with the launch of its first fund. Since then, GreenSky has focused on backing early-stage Canadian tech startups, raising smaller VC funds from LPs more often (typically once every two years) than many of its peers.

Hoffmann, who joined GreenSky last year for Fund V, will co-lead GreenSky’s investment efforts for Fund VI alongside List and partner Neil Peet.

Including this initial $15 million for its sixth fund, GreenSky has now raised a total of approximately $70 million to date. Broken down by fund, that is: Fund I ($3.1 million), Fund II ($5.1 million), Fund III ($8.4 million), Fund IV ($17.2 million), and Fund V ($21 million), which GreenSky finished deploying a few months ago.

Across its six funds to date, the VC firm has invested in 31 Canadian tech startups in total including Captain AI, Direct-C, Funnelytics, Mesosil, Micharity, Mission Control, Ontopical, PhenoTips, ProNavigator, Pulse Industrial, Symboticware, and WiseDocs.

GreenSky’s Fund VI LPs include ex-Research in Motion chief information officer and Virgin Mobile Canada CTO Valdis Martinsons (who now works as GreenSky’s chief technologist) and former Ontario Teachers’ Pension Plan investment committee chair Bill Chinery (who now sits on GreenSky’s investment committee).

“I met GreenSky when we were separately pursuing an early-stage tech investment,” Chinery said in a statement. “GreenSky’s diligence process so impressed me that I joined the investment committee. My early-stage investment portfolio is now run exclusively through GreenSky.”

RELATED: Mesosil secures $2.2 million to develop infection-fighting biomaterials for medical devices

Hoffmann acknowledged that the fundraising process has been slow for GreenSky, but said things “felt far worse” when it set out to raise Fund V in late 2022. Given GreenSky’s past performance and the interest it has seen to date, including a high degree of support from existing backers, Hoffmann is confident the VC firm will hit its Fund VI target later this year.

After many LPs invested heavily in Canadian VC when the market was hot, investors have become more cautious and selective amid the tech downturn, which has led to smaller funds and longer fundraising timelines for the VC firms that invest directly in Canada’s tech startups. According to RBCx, the first half of this year put 2024 on pace to see the fewest total dollars allocated to Canadian VC funds in a decade. Since then, things have picked up a bit with Radical Ventures’ $800-million USD AI growth fund among other recent VC fundraises.

“We’re lucky enough that we’ve been able to continue to have exits [and] return capital to our investors,” Hoffmann said. As GreenSky’s fourth and fifth funds are so recent, Hoffman pointed toward data on the performance of the VC firm’s first three funds.

Across this group, GreenSky claims that as of June 2024, all of the firm’s portfolio companies have raised follow-on funding, its DPI is 212 percent, its annualized internal rate of return (IRR) is 26 percent, and its total value to paid-in capital (TVPI) is 2.9x. This includes four exits, including Akira Health, Cyclica, Mirexus Biotechnologies, and Rank Software, and only one company failure.

Cyclica was acquired by American biotech Recursion last year for more than $53 million. GreenSky received shares in Recursion, which it held for a period and then sold for a profit in what Hoffmann described as a successful exit.

GreenSky’s performance has steadily improved with each of its first three funds according to data shared with BetaKit. For Fund I, the firm has posted 88 percent DPI, 7 percent IRR, and 1.79x TVPI. With Fund II, GreenSky has generated 183 percent DPI, 20 percent IRR, and 2.49x TVPI. For Fund III, GreenSky has posted 277 percent DPI, 63 percent IRR, and 3.61x TVPI.

According to a recent BDC report on Canada’s VC landscape, those DPI, IRR, and TVPI figures for GreenSky’s second (2017 vintage) and third (2019 vintage) funds place the firm beyond the upper quartile of Canadian VC funds from that timeframe in terms of performance. BDC reported that the average upper quartile DPI, IRR, and TVPI for funds from this period was 37 percent, 12.7 percent, and 1.37x, respectively.

Perusing Carta’s recent VC fund performance report shows that GreenSky’s metrics also appear competitive with US VC funds of the same vintage.

Hoffmann views GreenSky’s focus on deep tech companies, which typically develop products based on significant scientific or engineering innovations that can be tougher to evaluate than conventional software solutions, as a differentiator relative to other Canadian VC firms. She noted that GreenSky has been investing in deep tech for close to a decade and successfully exited multiple startups in the space, including Cyclica.

She also believes GreenSky’s alignment with its LPs—by being “heavily invested” alongside them—has been beneficial: across its first five funds, approximately 25 percent of invested capital came from the GreenSky team and family members.

RELATED: Fading 2023 VC performance underscores Canadian tech market’s “vulnerability,” BDC reports

For Fund VI, GreenSky has brought on former Verstra Ventures associate Justin Dunnion as senior associate to source deals and assist with due diligence. Hoffmann noted GreenSky is also shifting to doing one capital call this year, one in 2025, and one in 2026. “In our investors’ minds, it can be like, ‘Okay, that’s our allocation to VC for the next couple years,’” she said.

GreenSky plans to write $1.5-million to $2-million initial cheques for Fund VI, out of which it has already made four investments, backing Botni.vision, Brickeye, Edgecom, and Ethica Channel Enablement.

Hoffmann said GreenSky also recently exited a company she declined to name from its fourth fund for a return just above the amount it invested after that investment did not go as planned and it was approached by another VC that wanted to buy its stake. While this outcome was not the “home run” the firm initially sought, Hoffmann said it also wasn’t a failure, arguing that it illustrates the approach GreenSky has taken to managing its portfolio.

“Venture is a very bifurcated investment profile, where you get [a] few big wins and then most else [are] failures, but we are not just focused on getting the really big wins,” Hoffmann claimed. “We do think that if we can minimize the number of failures, that’s one way you could really contribute to growing attractive long-term returns.”

Feature image courtesy GreenSky Ventures.