A new report shows venture capital (VC) investments in Canadian tech last year grew slightly compared to 2023, buoyed by later-stage megadeals while seed-stage funding continued to struggle.

Megadeals—raises over $50 million—accounted for 62 percent of all dollars invested in 2024.

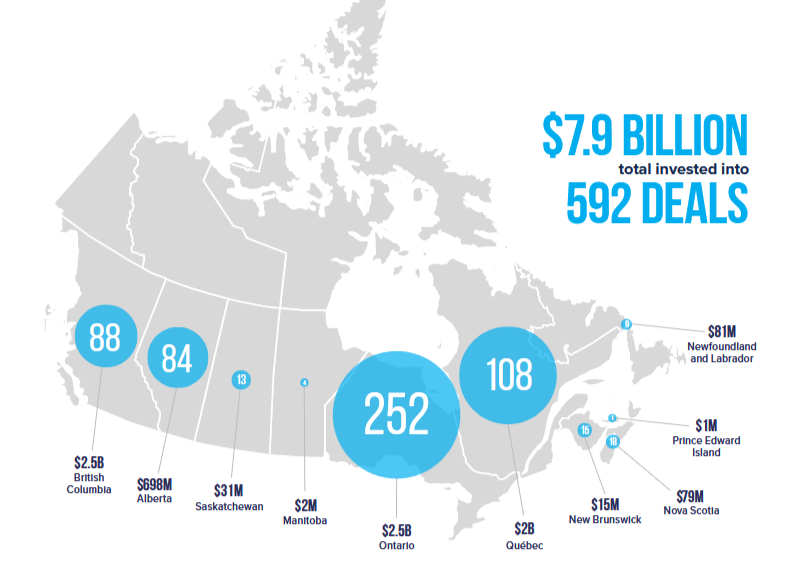

In its year-end market overview, the Canadian Venture Capital Association (CVCA) tracked $7.86 billion (all figures in Canadian dollars) invested across 592 deals in 2024, a roughly 10-percent increase in dollar value. But without Vancouver-based legaltech firm Clio’s $1.24-billion Series F round, the total amount invested nationwide would have dropped by six percent year-over-year.

The latest numbers from the end-of-year report mirrored those of Q3 2024: outlier deals, such as Clio’s, accounted for a significant portion of VC activity in Canada. Meanwhile, seed-stage funding rounds dropped by nearly half compared to the year before.

Q4 saw the fewest transactions and second-lowest value invested of the year, which the report noted is a common trend for the year’s final quarter. However, it marked the poorest Q4 performance since 2020, amid a climate of economic and political uncertainty in Canada.

Clio ensures BC is on the Best Coast

Clio’s outsized contribution indicates a larger trend in megadeals propping up Canadian VC last year. Megadeals—raises over $50 million—accounted for 62 percent of all dollars invested in 2024. Q4 added $701 million in megadeal transactions to the year’s total.

Despite a drop in deal count compared to 2023, the average deal size grew by 30 percent year-over-year, up to $13.3 million. Clio’s Series F, Cohere’s $616-million Series D, Blockstream’s $289-million convertible note financing, and Waabi’s $275-million Series B all boosted this metric.

Clio’s round also buoyed the standing of its home province of BC. More than three-quarters of all VC transactions took place in Ontario, Québec, and BC in 2024, and these provinces accounted for 88 percent of all dollars invested.

RELATED: Clio boosted Canadian VC investment in Q3 2024, but early-stage funding reaches “worrisome” low

Ontario took the top spot with $2.5 billion raised across 252 transactions. However, BC nearly matched Ontario’s dollars invested for the first time ever despite only closing 88 deals, again due to Clio totalling roughly half of the dollars raised in the province. Québec followed with $2 billion invested across 108 deals.

BC’s 2024 performance was not mirrored by the Atlantic provinces, which saw their deals cut in half compared to 2023, except for Newfoundland and Labrador—a disappointing downturn following a landmark year for Nova Scotia in 2023.

Series A Crunch or Seedpocalypse?

CVCA president and CEO Kim Furlong noted in the report that the overall uptick in VC funding was “a solid performance driven by key late-stage transactions.” However, she noted that the low seed-stage deal count “presents concerns about the long-term pipeline of high-growth startups.”

Seed transactions in 2024 saw $510 million deployed across 201 deals, dropping by 47 percent compared to the year before. The poor seed-stage performance continued a trend that Furlong called “worrisome” in the fall. When reached for comment by BetaKit, Furlong reinforced that concern, adding that low pre-seed and seed numbers could have “long-term implications for Canada’s competitiveness in emerging sectors.”

Matt Cohen, founder of Ripple Ventures, told BetaKit that “dollars invested are only one part of the story,” especially as Canadian companies focus on capital efficiency and revenue.

“It’s a sometimes misleading judgment of the health of the market,” Cohen said, noting that many pre-seed deals in Canada go unreported.

Cohen said that the pipeline of companies moving from seed stage to Series A funding rounds could represent a greater cause for concern.

RELATED: BDC Capital targets late-stage tech companies with nearly $1 billion in new fund commitments

The top Canadian VCs investing at the seed stage were the Golden Triangle Angel Network (GTAN), the Centre for Aging + Brain Health Innovation (CABHI), and the Business Development Bank of Canada (BDC)’s venture arm.

Yesterday, BDC Capital announced nearly $1 billion in funding for later-stage companies through direct investment funds, citing a market need for growth investments. In 2024, BDC Capital participated in 18 seed rounds, 30 Series A or B rounds, and 13 later-stage deals, but deployed the most capital at the Series A and B stages.

The most active VC funds in 2024 by dollars invested were all government-backed or pension funds.

Furlong expressed support for BDC’s new funding commitments, noting that later-stage support is crucial to ensuring that companies scale in Canada.

“Ensuring these high-performing firms have access to capital and strategic resources is crucial to keeping them headquartered in Canada,” Furlong wrote in an email to BetaKit. “BDC’s recent $1-billion commitment to late-stage investment is a significant step in this direction.”

However, the most active VC funds in 2024 by dollars invested were all government-backed or pension funds: BDC, Export Development Canada (EDC), Fonds de solidarité FTQ, and Investissement Québec. BDC ranked first overall both in deal count and dollars spent for 2024—a showing unlikely to change in 2025 given its new commitments.

As for private firms, Lumira Ventures, Portage Ventures, and Diagram Ventures led the pack in terms of dollars invested. The private firms that closed the most deals included the GTAN, Startup TNT, and CABHI.

US investors continued a strong post-pandemic streak, leading participation in 32 percent of all VC deals in Canada, despite dropping by two percent year-over-year. Notably, Clio’s Series F round was backed entirely by American investors.

Those US investors continued to provide capital to the Canadian ecosystem amid what was on track to be the worst VC fundraising year in a decade. According to CVCA Intelligence data, Canadian VCs raised $2.3B across 38 funds in 2024, roughly on par with 2020 levels.

When asked whether 2025 will bring an increase in Canadian VC fundraising, Furlong said that markets do not respond well to economic uncertainty, but that it was “impossible to forecast.”

Fusion acquisition provides life sciences boost

The Information, Communications & Technology (ICT) sector got the lion’s share of money invested, reflecting a multi-year trend, with $4.5 billion across 285 deals, despite deal count in the sector dropping year-over-year. The largest portion went towards internet software and services, followed by non-internet software and e-commerce.

Cleantech narrowly missed second place, garnering $1.1 billion across 58 deals and earning the highest average deal size of $18.4 million. BC led the provinces in cleantech deals, with 15 transactions.

Life sciences continued on a strong multi-year streak, netting the second-highest level of dollars invested in the sector on record. VCs invested $1.4 billion across 128 deals, a 15-percent increase compared to 2023.

The life sciences sector, which saw the most activity in Ontario, Québec, and Alberta, also boosted a sleepy Canadian exit landscape. AstraZeneca’s $3.26-billion acquisition of Fusion Pharmaceuticals was the largest exit of 2024, accounting for 63 percent of all exit value for the year.

Canadian exits dropped in 2024, with investors netting $5.2 billion across 40 exits, the vast majority of them mergers and acquisitions (M&A). This represented a downturn from 2023’s “record” year for M&A. The Canadian IPO dry spell continued, with not a single company going public.

Cohen said that he expects to see more US acquisitions of Canadian companies in the next year, regardless of the economic uncertainty created by the US tariff threat.

“No matter what the dollar is or tariff talk, there’s always been an appetite to acquire Canadian R&D talent and full acquisitions,” Cohen said.

Feature image courtesy Unsplash.