Toronto-based FinTech startup Koho Financial is targeting the roughly one-third of Canadians who rent with three new offerings.

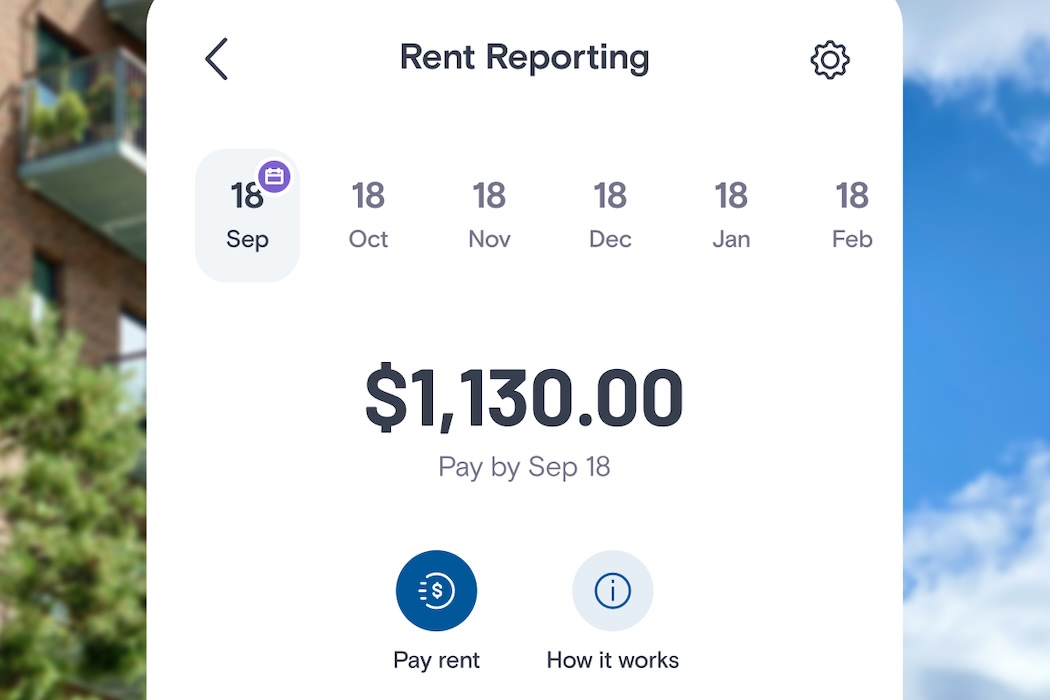

Today, Koho is introducing rent reporting to help its users build credit history, earn cash back on rent, and get tenant insurance through a partnership with Walnut Insurance. In an interview, Koho CEO and founder Daniel Eberhard told BetaKit that although many of Koho’s users are renters, this marks the company’s first dedicated offering specifically for them. Koho’s core product is a prepaid account for everyday spending and savings that allows users to make purchases with a Mastercard.

Koho CEO Daniel Eberhard said two-thirds of users who sign up are using Koho as their primary financial account.

With its new rent reporting feature, both new and existing Koho customers who pay rent through the platform will have their rent payments reported directly to a credit bureau. The idea is that for those who consistently pay their rent, this feature can become a valuable tool for building credit history.

Eberhard sees rent reporting as a way to turn the simple act of paying rent into a credit-building tool, not unlike a mortgage or credit card.

“Housing affordability is not a new issue in Canada,” he told BetaKit. “I think the historic ways that folks built credit were A, flawed, and B, out of reach.”

“The entry level way to build credit [through] a consumer unsecured credit card—which charges 18 to 22 percent [interest]—is really expensive and not a good product for a lot of people. I think that’s normalized and socialized in a way that does not make sense,” he added.

Besides using a credit card, Canadians can build credit through timely mortgage payments, but for renters, this simply isn’t an option.

With Koho’s rent reporting feature, users can sign up and continue making rent payments through their Koho account—no extra monthly steps or reporting are needed, according to Eberhard. The reporting also comes at no extra cost to users.

It’s a slightly different approach than that of fellow Toronto-based FinTech firm Borrowell, which also focuses on credit building and shares an investor with Koho. Borrowell’s Rent Advantage feature lets tenants report rent on a monthly basis for $8 per month. The service also allows users upload up to two years of their previous rent payments to Equifax Canada to build their credit history.

The case for linking rental payments to Canadians’ credit scores has gained momentum this year. In the spring, the federal government proposed factoring timely rent payments into credit score calculations. Supporters of the proposal argue that it could help aspiring homeowners build the financial credibility needed to qualify for a mortgage or secure better borrowing rates.

Critics, on the other hand, warn that it could harm the credit scores of those who struggle to pay their rent on time in the context of high housing costs.

“That’s a silly argument,” Eberhard said, pointing out that such an outcome would simply indicate “the system working.”

“The point is, if you are a responsible rent payer, that should be reflected in your credit score …to me, that’s a feature, not a bug,” he added.

He explained that rent reporting is Koho’s effort to reach a point where everyday or “natural behaviours,” like paying rent, play a bigger role in building credit history compared to “unnatural” ones, such as relying on unsecured debt.

There appears to be strong early interest in the rent reporting product—Eberhard claimed that over 7,000 people signed up in the first week of its “dark launch,” which started July 30.

Along with rent reporting, Koho is offering eligible renters 0.25 percent cash back on every rent payment made through the Koho platform, automatically deposited into their Koho account. Koho isn’t the first in Canada to link rent to rewards—Toronto-based Chexy also allows users to split rent with roommates and earn cash back or rewards by paying rent with a credit card. It also offers rent reporting to help its customers build their credit history.

The third component of Koho’s new offering for renters is tenant insurance, provided through a partnership with Toronto-based Walnut Insurance. The service is available to users in Alberta, British Columbia, Manitoba, Nova Scotia, and Ontario who are using the rent reporting product.

RELATED: Walnut Insurance secures $4 million CAD to help FinTechs deliver embedded insurance programs

Founded in 2020 by serial entrepreneur Derek Szeto and growth specialist Adrien Niblock, Walnut helps brands deliver their own insurance offerings. Rates for the tenant insurance plan offered by Koho and Walnut start at $22 per month. Eberhard declined to disclose how Koho profits from this arrangement.

While all three new products were created with renters in mind, Eberhard said they also offer potential benefits for landlords.

Landlords “should care about” their tenants and want to help them build their credit history, he said. “Hopefully that makes you more competitive as a landlord in getting tenants, but then also it makes it easier for them to have a reliable tenant insurance product, so that you don’t have to worry about that as a landlord either.”

Credit building has become one of several core focus areas for Koho. Eberhard said currently, two-thirds of users who sign up are using Koho as their primary financial account.

Koho has traditionally relied on partnerships with regulated third parties to deliver many of its products. However, earlier this year, the company revealed that it’s working with Canadian regulators to obtain a Schedule 1 banking licence. Eberhard told BetaKit in January that he hopes this move will mark the beginning of an opening in Canada’s “deeply uncompetitive” financial services market.

Eberhard said Koho is still “very active and on track,” with that process. In the meantime, Koho has been focused on balancing growth with reaching profitability.

Last year, the company restructured its team, which included two rounds of layoffs—though the company was still hiring—to better allocate capital towards growth initiatives, according to Eberhard. To further service that goal, the company raised $86 million CAD in a Series D extension in December 2023.

Koho has more in store on its product roadmap, including a buy now, pay later tool that’s currently in beta.

Regarding its growth goals, Eberhard claimed that Koho’s revenue has increased by roughly 80 percent year-over-year, with the company now “well north” of the $100-million run rate it announced after raising its Series D extension.

“We continue to be very focused on winning core accounts and primary financial behaviour,” he said, adding that Koho is focused on making its product “the best account in the country for the folks that we think we’re best equipped to help.”

Feature image courtesy of Koho.